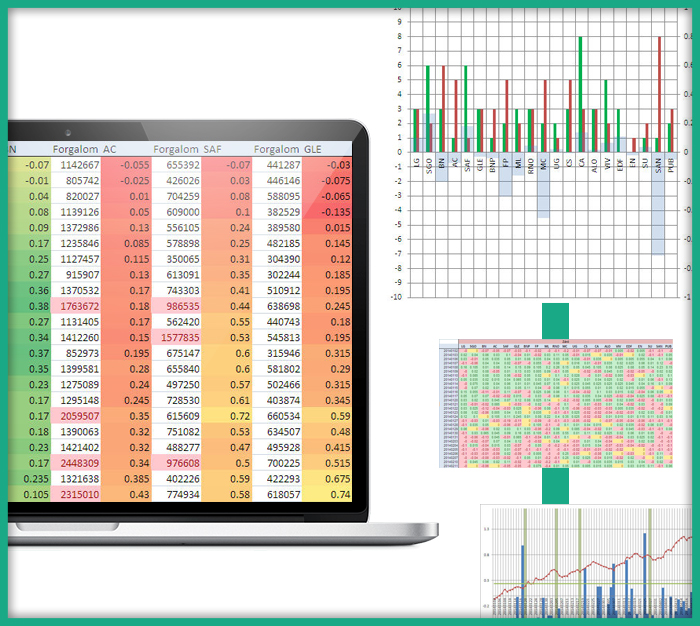

Stock screener

Aim: To develop a stock screener and decision-making support system which helps domestic medium- and long-term investors to make decisions.

We have developed the first stock screener and decision-making supporting system in Hungary which collects the EOD marks of more than 15,000 instruments on the NYSE, NASDAQ, XETRA, ASK, and BÉT (Budapest Stock Exchange). The screening is based on the share price, its volume, the signals of indicators and the recognition of candle formations. The system can calculate the trend and regression lines, the channels, and their difference from the mean within milliseconds. Trading signals of indicators received special attention and the software can follow 20 indicators’ values, process and interpret the results. With the system, one can quantify the momentum of the stock, the strength and size of the trend, the size of the volatility, and the volume indicators. The stock screener system can identify 90 candle formations. Therefore users are able to trade specific patterns, but one can define groups - such as reliability or expected trend - as well. Users can customise their trading strategies, and can monitor its expected success based on historical data. The programme assembles the results list based on current trading signals, using technical analysis tools.